SEAFDEC Southeast Asian Fisheries Development Center

SEAFDEC Southeast Asian Fisheries Development Center

By Jennifer Viron, 2019 Regional Fisheries Policy Network (RFPN) Member for Philippines

INTRODUCTION

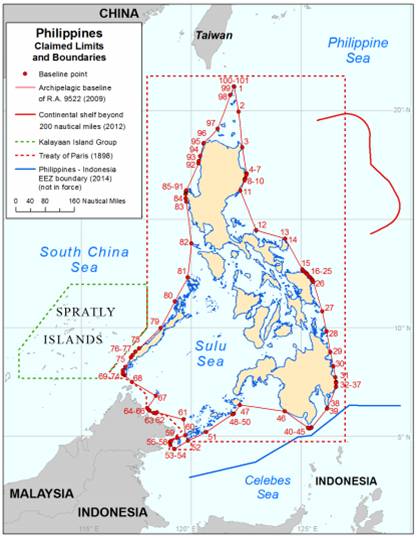

The Philippines is located within the coral triangle, which dubbed the archipelagic country as the center of the center of marine biodiversity (Carpenter and Springer, 2005). The country has a total land area of 301,000 km2 and has a coastline of 36,289 km. It is surrounded by major bodies of water such as the Pacific Ocean in the east, South China Sea in the west, Luzon Strait in the North, and Celebes Sea in the south. The surrounding territorial waters, with the promulgation of the exclusive economic zone (EEZ) and the United Nations Convention on the Law of the Sea (UNCLOS), is about 2.2 million km2 (BFAR, 2018) (Figure 1).

FISHERIES SECTOR

One of the major sources of livelihood in the country is fishing and most of the fishers are involved in capture fishing while others are involved in aquaculture, vending, gleaning, and processing. In 2018, the contribution of the fisheries sector to the gross domestic product of the country was 1.2 % and 1.3 % at current and constant prices, respectively. Out of the estimated population of 105 million people, about 82 million are fish eaters and each one consumes about 38.2 kg of fish per year (BFAR, 2018).

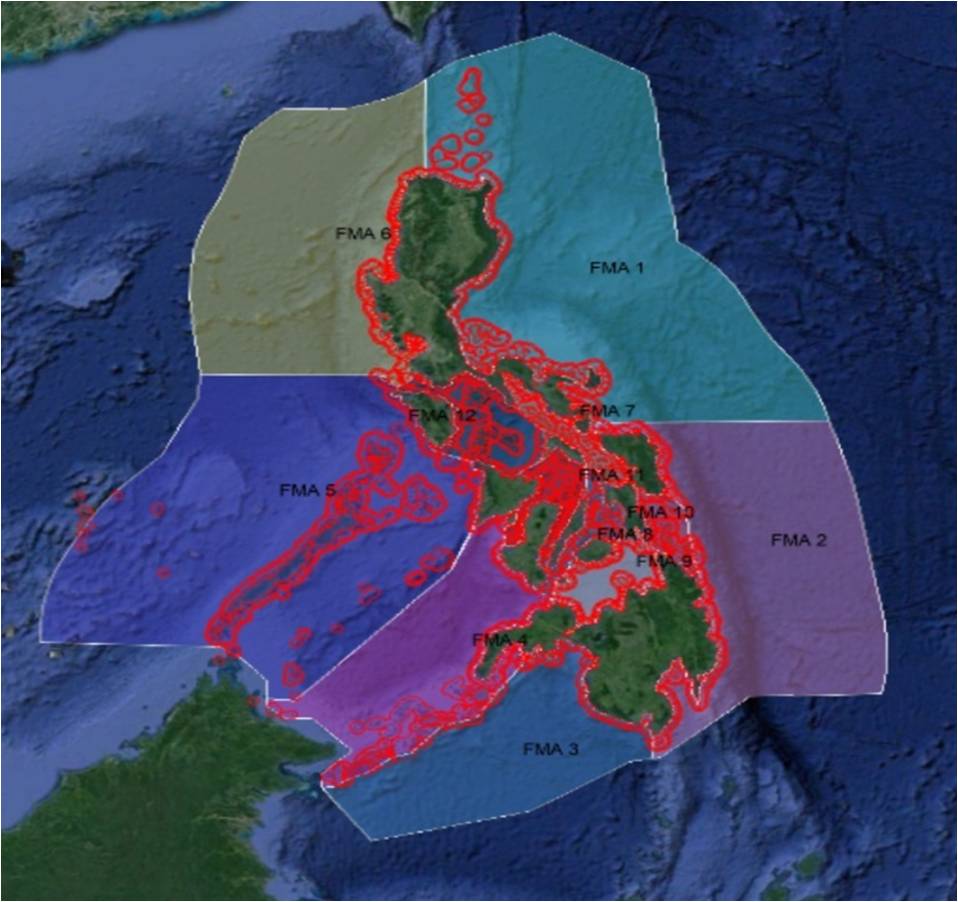

The Bureau of Fisheries and Aquatic Resources (BFAR), under the Department of Agriculture, is the government agency responsible for the development, improvement, management and conservation of the Philippines’ fisheries and aquatic resources. In 2019, a total of 12 fisheries management areas (FMAs) (Figure 2) were established under the Fisheries Administrative Order 263 Series of 2019 to ensure sustainable fishery resources by promoting management based on the status and capacity of stocks as well as promote co-management among BFAR and LGUs.

The fisheries sector of the Philippines is categorized into commercial, municipal, and aquaculture. Commercial fisheries refers to capture fishing operations using vessels of over 3 GT outside the municipal waters (beyond 15 km from the shoreline) and should secure commercial fishing vessel license from BFAR which is subject to renewal every three years. Municipal fisheries is under the jurisdiction of the local government units (LGUs) and refers to capture fishing operations using boats of 3 GT or less including other forms of fishing not involving the use of water craft. Aquaculture involves fish culture activities in inland and marine waters.

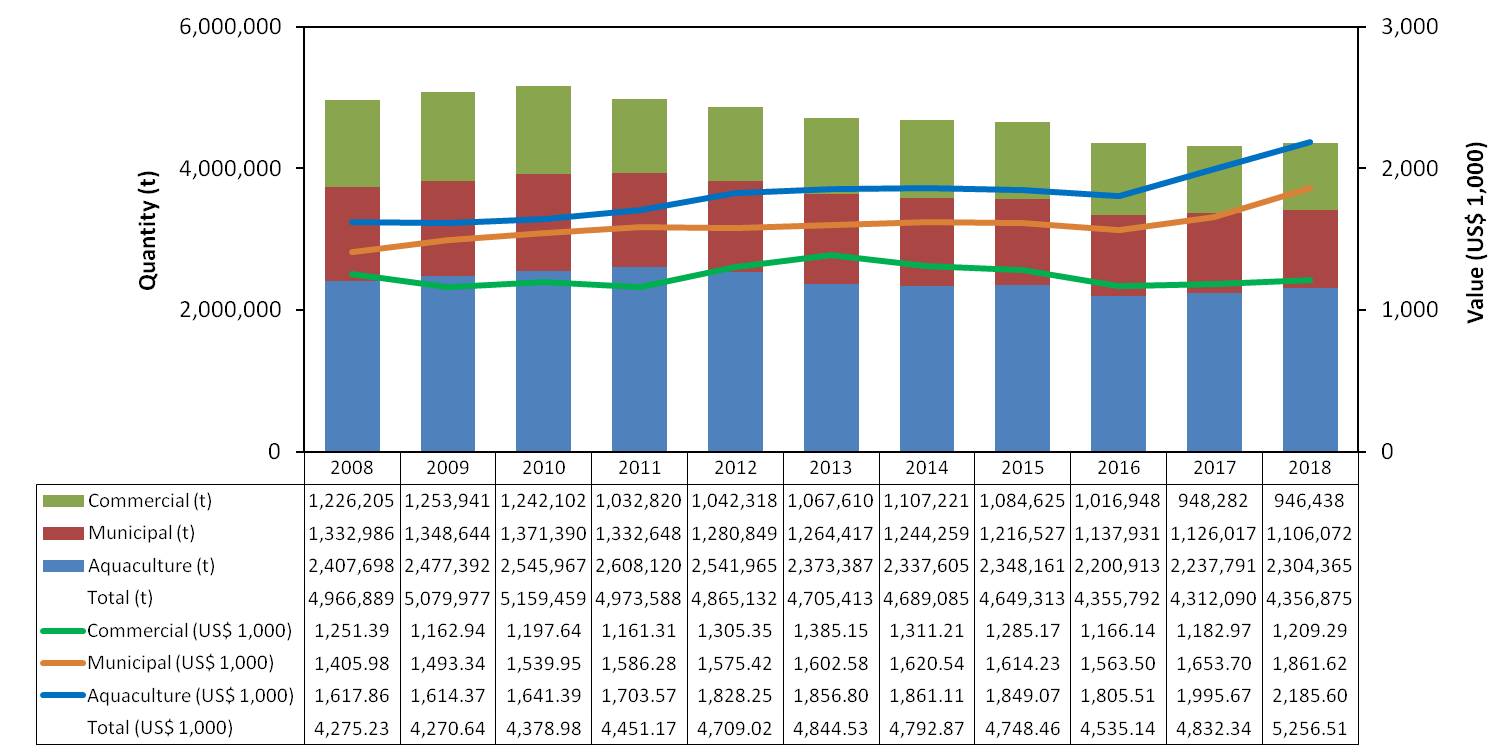

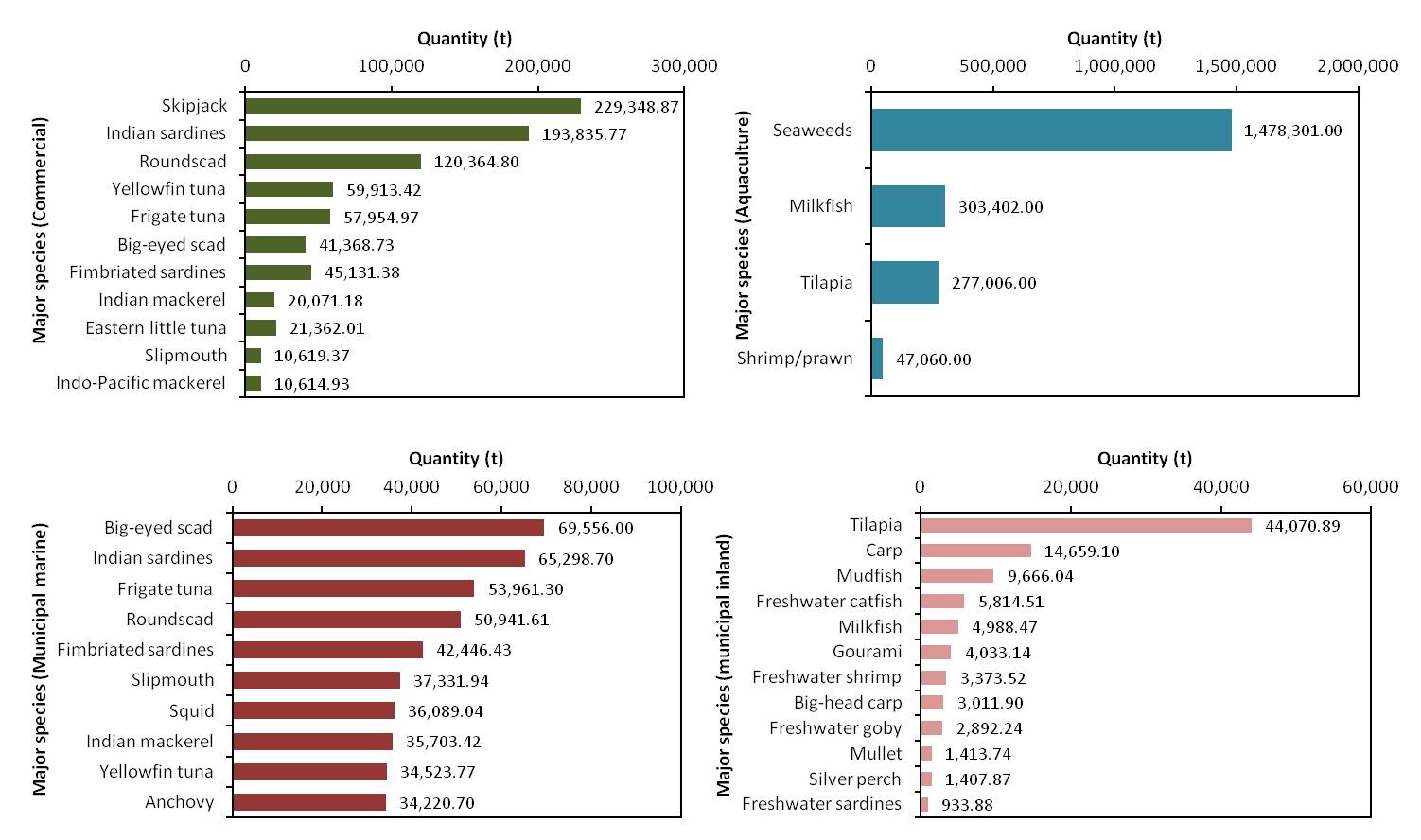

In terms of world ranking in total fish production, the Philippines was constantly among the top 10 for several years. In 2008-2010, there was a constant increase in the volume of total production, however, the volume gradually decreased from 2011 to 2018 (Figure 3). In 2018, the total volume of fisheries production was 4.36 million t with the value of about US$ 5.26 million. The production volume of major species of each fisheries sub-sector is shown in Figure 4.

FISHERIES TRADE

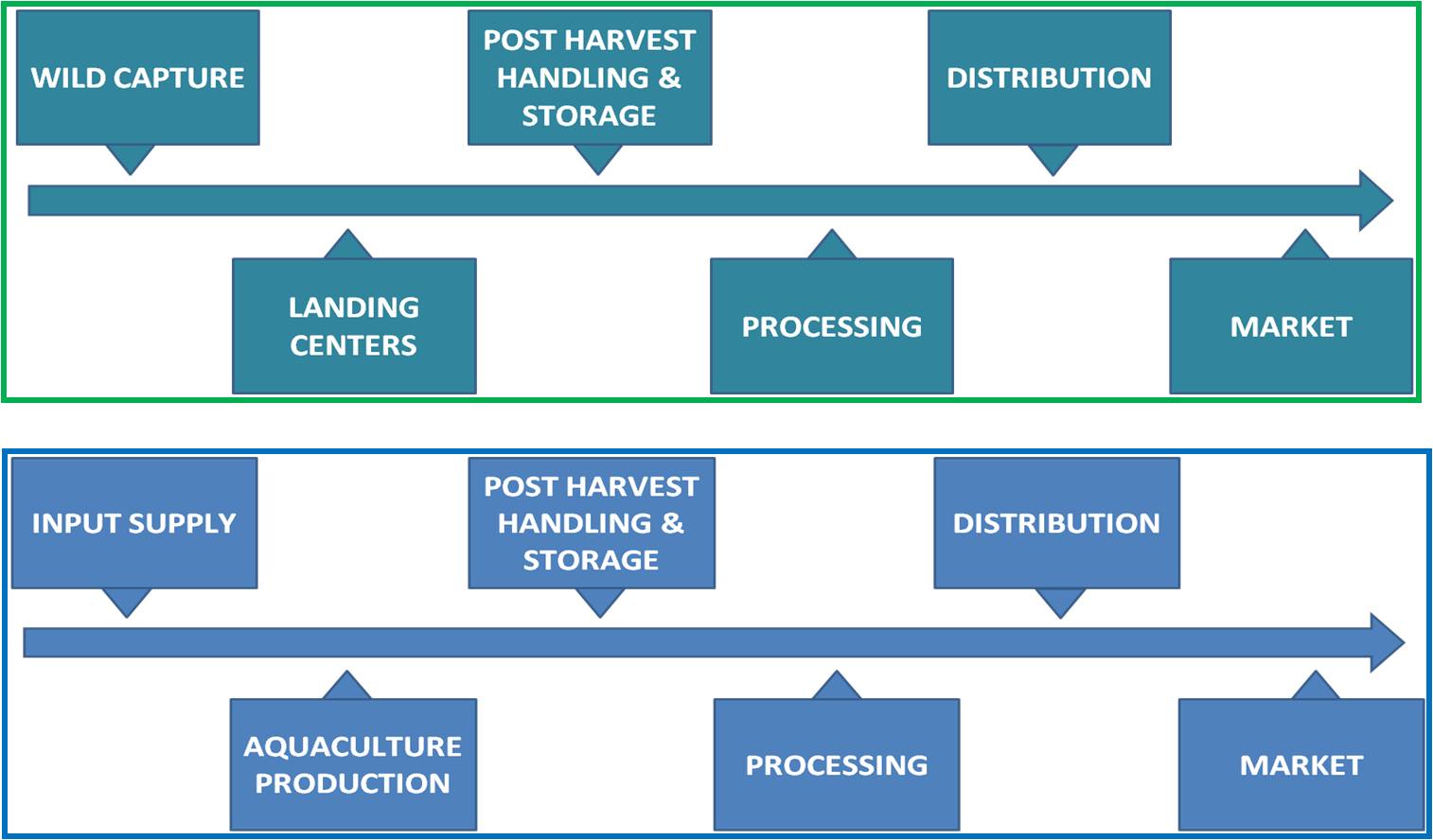

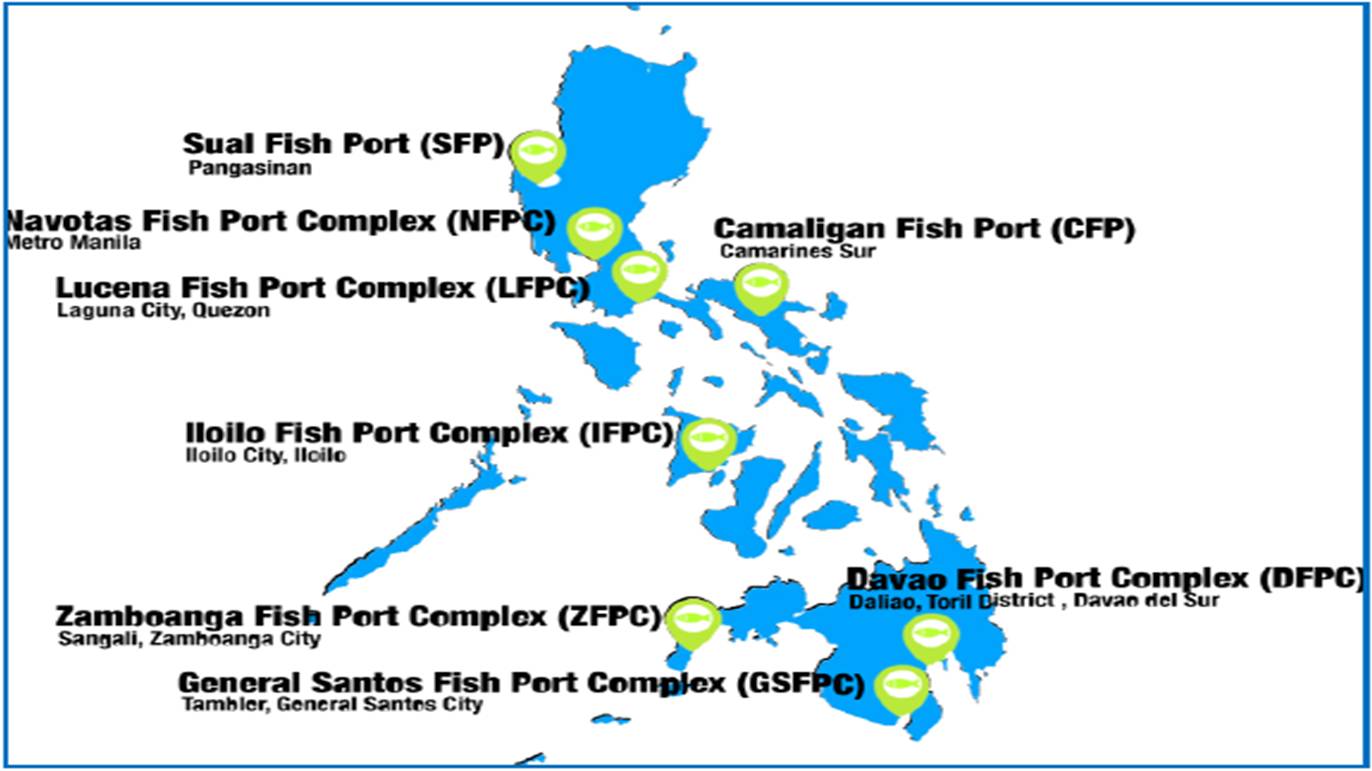

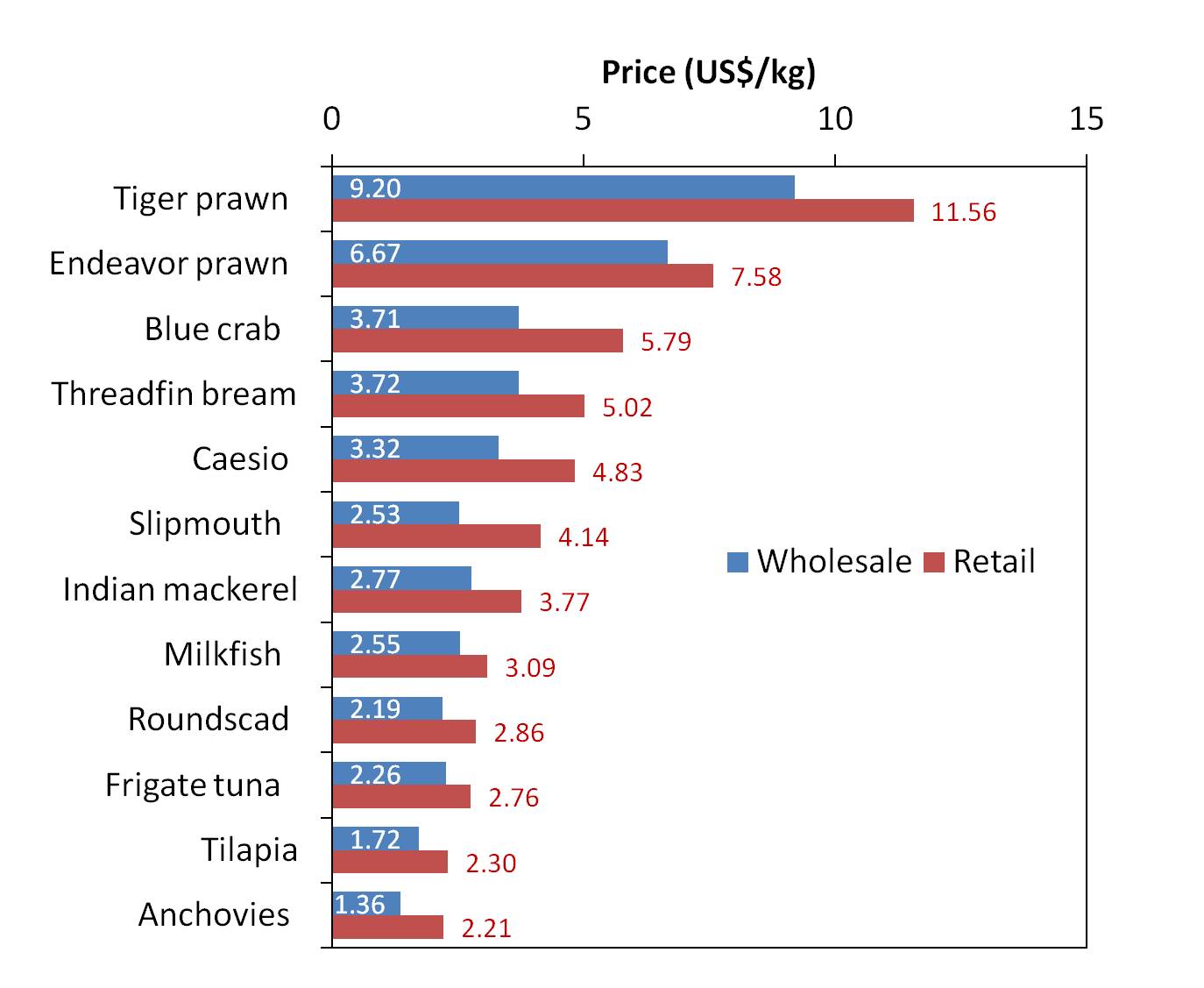

The fish and fishery products from capture fisheries and aquaculture undergo post harvest handling and processing before ending up in markets (Figure 5). The eight major fish ports (Figure 6) in the country are managed by the Philippine Fisheries Development Authority. Designed for unloading and marketing of marine fish and fishery products both for local and foreign markets, the operations of the General Santos Fish Port Complex cater to tuna hand line boats, purse seiners, and huge capacity refrigerated foreign vessels and it is equipped with processing and refrigeration facilities (PFDA, 2019). Furthermore, the wholesale and retail prices of selected fish species in the Philippines in 2018 showed an average increase of about US$ 1.0/kg which could be attributed to the tight supply of commodities globally and seafood trade in 2018 (Figure 7).

EXPORT OF FISH AND FISHERY PRODUCTS

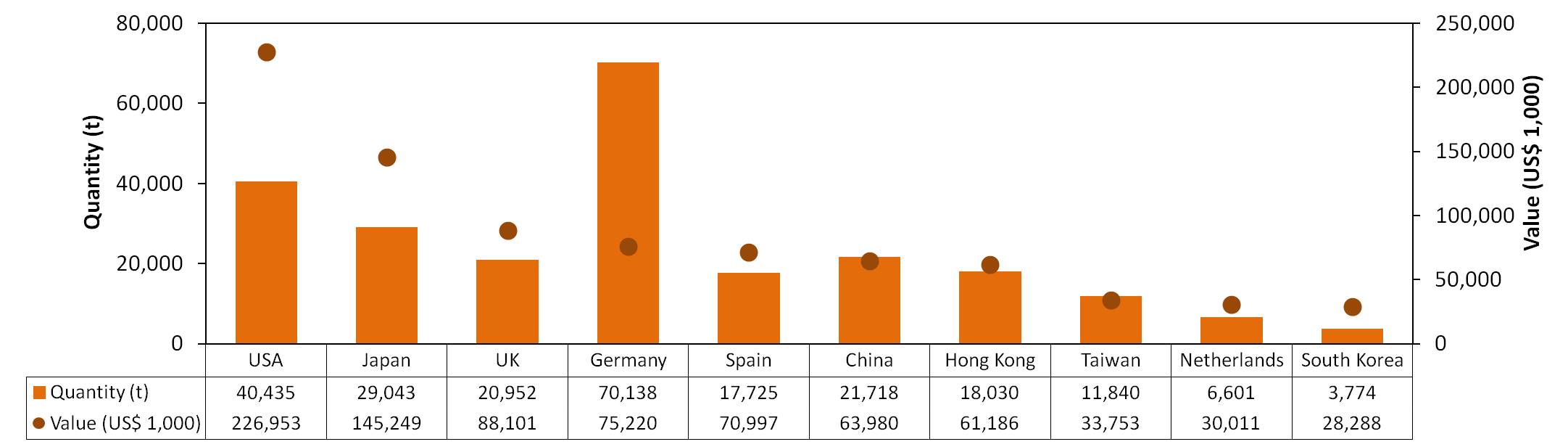

In 2018, tuna products (fresh, chilled, frozen, smoked, dried, or canned) were the top exported commodities with a volume of about 171,452 t valued at more than US$ 492 million. Other major fish and fishery products include seaweed, crab, shrimp/prawn, octopus, grouper, squid, sea cucumber, ornamental fish, and roundscad (Figure 8). The major countries of destination of exported fish and fishery products in terms of value include USA, Japan, UK, Germany, Spain, China, Hong Kong, Taiwan, Netherlands, and South Korea (Figure 9).

IMPORT OF FISH AND FISHERY PRODUCTS

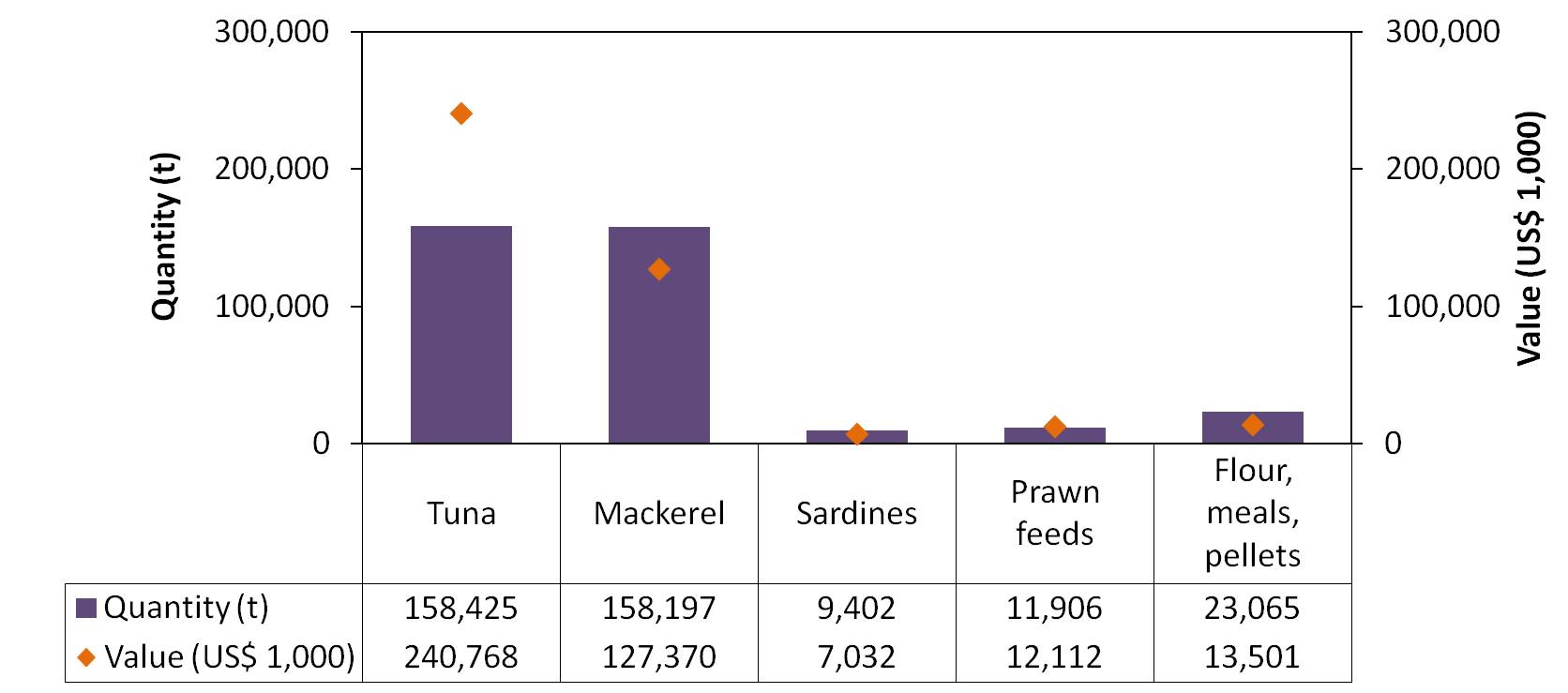

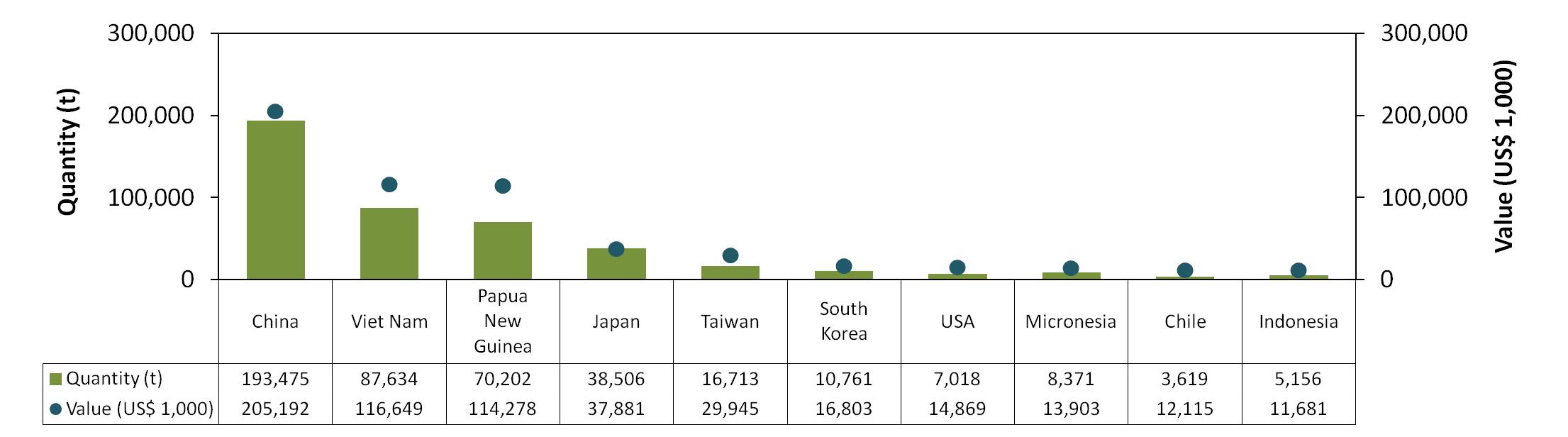

Tuna, mackerel, and sardines (fresh, chilled, or frozen) were the top commodities imported by the Philippines in 2018, followed by prawn feeds as well as flour, meals, and pellets of fish, crustaceans, and mollusks fit and unfit for human consumption (Figure 10). The top ten countries where imported fish and fishery products originated include China, Viet Nam, Papua New Guinea, Japan, Taiwan, South Korea, USA, Micronesia, Chile, and Indonesia (Figure 11).

MAJOR ISSUES ON FISHERIES TRADE

The following are the issues being faced by the domestic and international markets of the Philippines:

- Limited marketing networks for the distribution of products from highly productive areas to food-fish deficient areas

- Inadequate transport services which resulted to high cost of distribution of fish raw materials and products

- Outdated trading facilities

- Low marketability of fish and fishery products in terms of variety, labelling, packaging, etc.

- Unstable market prices

- Stringent and tedious export-import procedures

- Inability to comply with regulatory requirements for food quality and safety (e.g., standards of HACCP, US, EU, etc.)

LAWS ON FISHERIES TRADE

The following are the laws related to fisheries trade of the Philippines:

- DA Fisheries Administrative Order No. 221 Series of 2003 – Regulating the importation of live fish and fishery/aquatic products under FAO No. 135 s. 1981 to include microorganisms and biomolecules

- Republic Act No. 8550 – An act for the development, management, and conservation of the fisheries and aquatic resources, integrating all laws pertinent thereto, and for other purposes

- Fisheries Code of 1998 – Section 61. Importation and exportation of fishery products, Section 62. Trade-related measures, Rule 62.1. Standards, and Rule 62.2 Updating of trade related measures

INTERNATIONAL TRADE AGREEMENTS

The Philippines is a signatory of the following free trade agreements:

- Philippines-Japan Economic Partnership Agreement (PJEPA)

- Philippines-USA Trade and Investment Framework Agreement

- Philippines-FTA Agreement (with Iceland, Liechtenstein, Norway, and Switzerland)

- ASEAN-Hong Kong, China Free Trade Agreement

- Regional Comprehensive Economic Partnership

- ASEAN Free Trade Area

- ASEAN-Australia and New Zealand Free Trade Agreement

- ASEAN-India Comprehensive Economic Cooperation Agreement

- ASEAN-Japan Comprehensive Economic Partnership

- ASEAN-People’s Republic of China Comprehensive Economic Cooperation Agreement

- ASEAN-Republic of Korea Comprehensive Economic Cooperation Agreement

WAYS FORWARD

To address the challenges in the fisheries trade of the Philippines, the Comprehensive Post-harvest, Marketing and Ancillary Industries Plan (CPHMAIP) 2018-2022 adopted the trade and marketing goals of the Comprehensive National Fisheries Development Plan of the Philippines (CNFID 2016-2020) which is to increase the quantity and value of traded fish and fishery products for domestic and international markets. The CNFID 2016-2020 focuses on the enhanced marketing strategies in the regions with low fish sufficiency.

Moreover, the improved quality and compliance to international standards on food safety, traceability, packaging, increased participation in locally held and international trade fairs, strengthening fishery data collection and increased capacitated fishery-based micro, small, and medium enterprises (MSMEs) would allow for an over-all increase in fisheries trade over the years. The medium term 2016-2020 trade and marketing sub-sector identified the following major strategies to address the issues and challenges in fisheries trade:

- Ensure the availability of sufficient supply in food-fish deficient areas;

- Expand the market for sustainable fish and fishery products (domestic and export);

- Increase the number of capacitated and competitive fishery-based MSMEs that can enter the domestic and international markets;

- Establish a comprehensive market information system;

- Strengthen the enforcement of laws and policies and regulations related to fisheries trade and marketing; and

- Enhance the capacity and competency of fisheries institutions, human resources, and professionals in LGUs, NGOs, among others specific to fisheries marketing.

REFERENCES

BFAR (2018). Philippine Fisheries Profile 2018. Bureau of Fisheries and Aquatic Resources. Department of Agriculture. Quezon City, Philippines.

BFAR. (2019). Establishment of Fisheries Management Areas (FMA) for the Conservation and Management of Fisheries in Philippines Waters. Bureau of Fisheries and Aquatic Resources. Department of Agriculture. Quezon City, Philippines.

Carpenter, K.E. and Springer, V.G. (2005). The center of the center of marine shore fish biodiversity: the Philippine Islands. Environ Biol Fish 72, 467–480. Retrieved from https://doi.org/10.1007/s10641-004-3154-4

NAMRIA. (2012). National Mapping and Resource Information Agency. Retrieved from www.namria.gov.ph

PFDA. (2019). Philippine Fisheries Development Authority. Retrieved from www.pfda.gov.ph

ACKNOWLEDGMENTS

The author would like to thank the following who helped in accomplishing this Special Assignment for 2019 RFPN:

- staff of the Bureau of Fisheries and Aquatic Resources

- officials and staff of SEAFDEC Secretariat

- 2019 RFPN Members

ABOUT THE AUTHOR

Ms. Jennifer G. Viron is a Researcher at the Capture Fisheries Division of the Bureau of Fisheries and Aquatic Resources located at 3rd Floor PCA Building, Elliptical Road, Diliman, Quezon City, Philippines. She can be contacted at jennyviron@gmail.com.

SUPPLEMENTARY DATA

Supplementary Data: Philippines (click to download)